|

Astute investors accumulate solid prospects while

timing the trough in commodity cycles

Iron ore exploration and development mining companies

operate in a highly cyclical industry and their share

price is closely correlated with the prices of the

product they aim to bring to market. Successfully

advancing a deposit to market involves planning and

foresight by shareholders and management, with the

ability to see logistics and milestones through to the

next cycle. Sharp increases and decreases in the pricing

for the steelmaking raw materials (the marketable end

product of the deposit mined) impacts the volatility of

share price. Global

iron ore benchmark pricing, one of the main drivers

in determining the revenue for iron mines, appears low.

As such, the share prices of all miners in this sector

have followed the downward movement in iron ore pricing.

Importantly, the fundamentals supporting the long-term

strategy of most are intact despite the recent cyclical

decline in pricing, which is not expected to continue

for the longer term.

Below is an overview of a junior miner that has an

exceptional deposit with plans to advance toward a

low capex (targeting below $1B), low opex (targeting

$65/T (loaded)) mining operation scenario. It currently has ~$1 million in the

bank, has low overhead (requiring only ~$280,000/year

to keep the doors open, including salaries for key

professionals and shared office space (shared with other

mining venture)), and is currently arranging to close

financing that is expected to see it through to

meaningful development (see related July 23, 2014 news

release entitled "Lamêlée

Announces Pricing of Prospectus Offering"). This

junior has the hallmarks of a viable mine site, it has

enough room to develop a concentrator/process, it is

within 5 km of provincial roads, plus it has access to

land and wharf at nearby Port-Cartier to deliver its

product. The team tasked with advancing this junior

miner are the same individuals that started up the

Consolidated Thompson's iron ore operation at Bloom

Lake, they advance that project to buy-out, and in the

process they brought the stock of Consolidated Thompson

up to where they sold it for $17.25 per share in 2011

($4.9 billion) --

the plan is to replicate that success -- accumulating

shares of this company now appears wise.

|

Lamelee Iron Ore Ltd. (TSX VENTURE: LIR)

(Frankfurt: G11) is a Canadian mining company with a Québec property located

at the south end of the Labrador Trough. LIR.V has

an experienced team with

great track record, they successfully developed and brought to

production the Bloom Lake Iron Mine in Québec (2005-2010).

The Lamêlée Iron Ore deposit sits in the heart of Quebec’s and

Labrador- Newfoundland’s Fermont-Wabush-Labrador City Iron Ore

Camp where iron concentrate production is currently at 35

million tonnes per annum. |

Shares Outstanding

Major shareholder 1) Fancamp

Major shareholder 2) GimusInc. (base shares)

H/D Financing:

F/T Financing:

O/S Warrants

O/S Options

F/D Shares

Cash Position

Debt |

77,221,971

45,000,000

13,104,000

15,575,000

3,542,971

7,993,214

5,900,000

91,115,185

$1.0M

DEBT FREE |

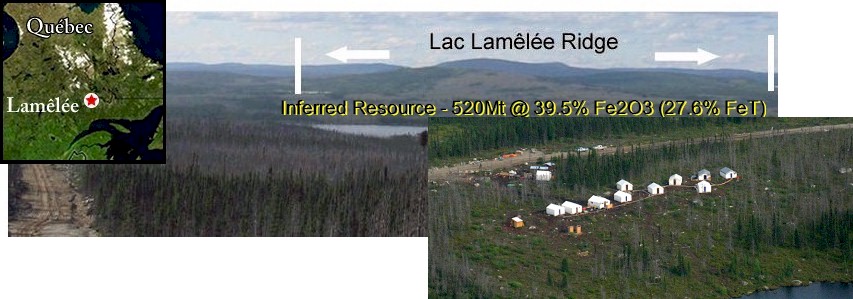

Figure 1. (above)

Location map (upper left inset), Lac Lamelee Ridge, containing the deposit

at Lamalee, Exploration camp at Lamalee (lower right inset)

-- The Project sits 10 km west/southwest of

Champion’s Consolidated Fire Lake North project.

The Objective

• To build the next iron mine at the southern end of the

Labrador Trough close to the Fermont Iron Ore camp.

• Pre-production is expected for Q4-2017.

The Plan

• To develop a 5-8M tonnes/year mining operation.

• To produce a low cost, high-grade iron concentrate.

• CapEX Below $ 1B

• Opex TARGET $65/T (loaded)

• Innovating mine to port solution.

• Efficient ship loading

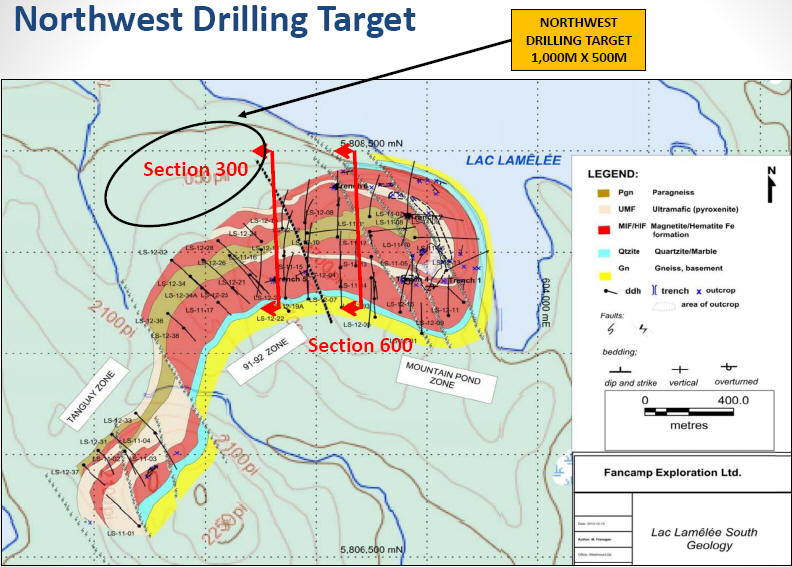

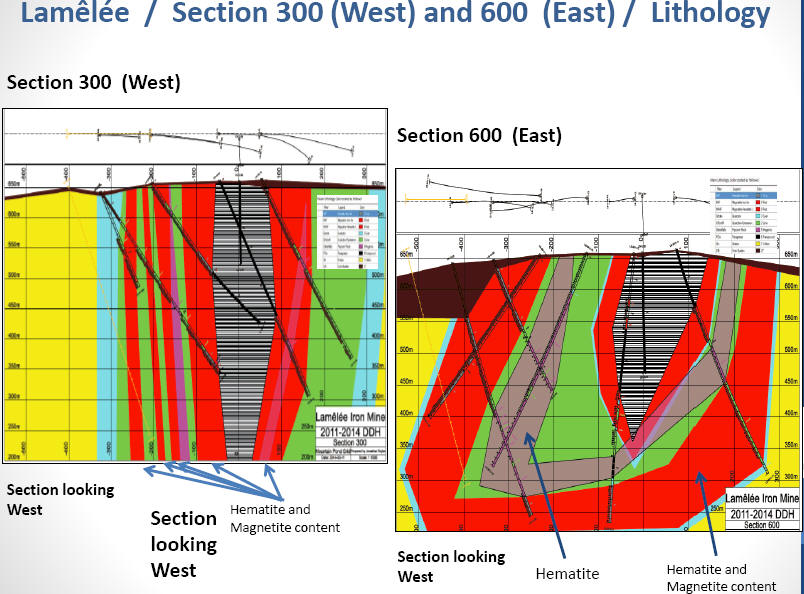

The Lamelee South deposit is interesting from an

economic point of view as it has a lot of iron formation

squeezed into a relatively small area, a study indicates

100% of the Inferred Resources are in the pit shell (the

area where the mining is expected to take place).

|

Resource

The Lamêlée

Iron Ore deposit contains, as of today, Inferred Mineral

Resources 520 million tonnes grading 39.5% Fe2O3 (or

27.6% FeT) - work to be completed in 2014 should

increase the size and the quality of the iron resources

towards 750 million tonnes at the same grade.

The following table outlines incremental

tonnages and Iron grades at various cut-off

grades:

The Whittle Open-Pit Shells Study

resulted in outlining two shells: the first

a smaller open-pit shell of 315 million tonnes at a grade of 41.2% Fe2O3 (28.8% FeT);

the second a larger open-pit shell of 520

million tonnes at a grade of 39.5% Fe2O3

(27.6% FeT). A comparison of results

demonstrates the amenability of the Inferred

MRE to potential open pit mining with 100%

of Inferred MRE reporting within a

conceptual open-pit shell.

Expectations of a highly economic mining operation

Lamêlée

Iron Ore expects a viable project producing 5-8 million

tonnes of concentrate. Using existing rail and new port

infrastructure, between $750 million to $1 billion in

capital costs and total operating costs between $60 and

$70 per tonne at a sustainable iron ore price of

$120-$130 CFR per tonne. |

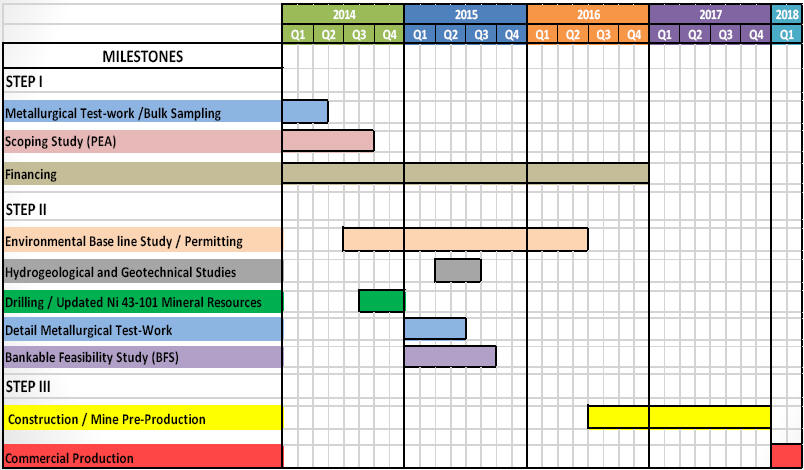

Plans

LIR.V plans to

conduct

metallurgical test work and produce a Preliminary

Economic Assessment (PEA) Study (using economic

parameters with a +- 30%) for delivery in

Q4-2014.

Financing

requirements:

•$3M to complete STEP I including additional drilling

and to initiate environmental assessment.

•$7M to initiate and complete STEP II in

2015.

Experienced team

Lamêlée

Iron Iron Ore will be managed and operated by members of

the team that brought the Bloom Lake iron deposit to

production within 4 years of the feasibility study. The

company was acquired for $4.9B at $17.25 per share.

Click here for CVs of Board of Directors.

No issues

Permitting

(environmental, socio-political, First Nations) will not

be an issue, since the processing technology follows

current industry standards (ie., water is used as the

main driver of concentration and there are no

deleterious elements in the iron ore); there is only one

First Nations group present in the Fermont area which

has dealt favorably with the Bloom Lake operation; and

Quebec’s and Labrador- Newfoundland’s

Fermont-Wabush-Labrador City Iron Ore Camp has a history

of iron mining since the 1960’s.

Deposit insight

Work

performed:

• Resource Modeling (57 DDH’s / 18,220m)

• 3-D mineralization

• Iron grade estimate

• Samples for future metallurgical test work

• Higher grade BIF’s -43% Fe2O3, hematite and magnetite

ore

• Geophysics program / Gravimetryand Mag Survey

Course hematite and magnetite -- the course grain lends

to the expectation to having a cost efficient process.

Preliminary specs show very good material with low

impurity.

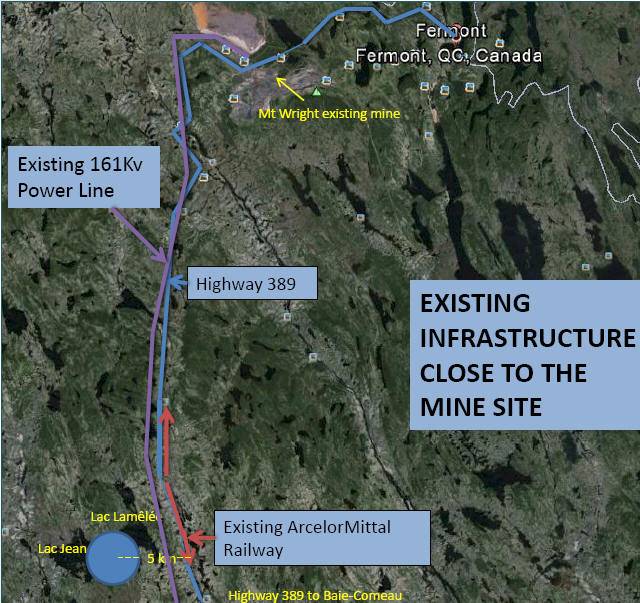

Infrastructure advantages

Port-Cartier layout

- note

proposed laydown area for LIR.V's material

Transshipment potential via Port-Cartier

Market Equities Research Group has identified the following related research

links on Lamelee Iron Ore Ltd.:

- Lamelee Iron Ore Ltd. Corporate Website:

http://www.lameleeiron.com

- SEDAR Filings for Lamelee Iron Ore Ltd.:

http://sedar.com/DisplayProfile.do?lang=EN&issuerType=03&issuerNo=00032549

# #

This release may contain forward-looking statements regarding future events that

involve risk and uncertainties. Readers are cautioned that these forward-looking

statements are only predictions and may differ materially from actual events or

results. Readers are cautioned that not until subject companies actually

releases official details themselves should anyone rely on the information

presented herein. Articles, excerpts, commentary and reviews herein are for

information purposes and are not solicitations to buy or sell any of the

securities mentioned.

Contact information:

Simon Levinson,

Editor in Chief

Market Equities Research Group

s.levinson@marketequitiesresearch.com

Fredrick William, BA Ec., f.william@marketequitiesresearch.com

|